How We Helped a DMCC Company Unlock Banking After Months of Struggle

When the client first approached us, it wasn’t just another business discussion. It was a conversation filled with frustration, uncertainty, and genuine distress. The client had done everything “by the book,” or so he thought.

The Beginning — A Common Yet Costly Situation

In September 2025, the client incorporated a company in the DMCC Free Zone. Following the advice of a consultant, he opted for a Flexi Desk setup, with plans to upgrade to a physical office later. This seemed like a practical approach, lower costs, faster setup, and flexibility.

However, when he tried to open a business bank account in Dubai, the responses from banks were discouraging:

- “Under review”

- “Not within our risk appetite.”

- “Please upgrade the office.”

- “We cannot proceed.”

Weeks turned into months, and even the consultant admitted that they couldn’t secure a corporate bank account in the UAE. Meanwhile, the business couldn’t operate, clients were waiting, costs were accumulating, and pressure was building. By January, nearly five months later, the company was still without banking. That’s when the client turned to us for DMCC banking assistance.

What We Saw — Beyond the Surface

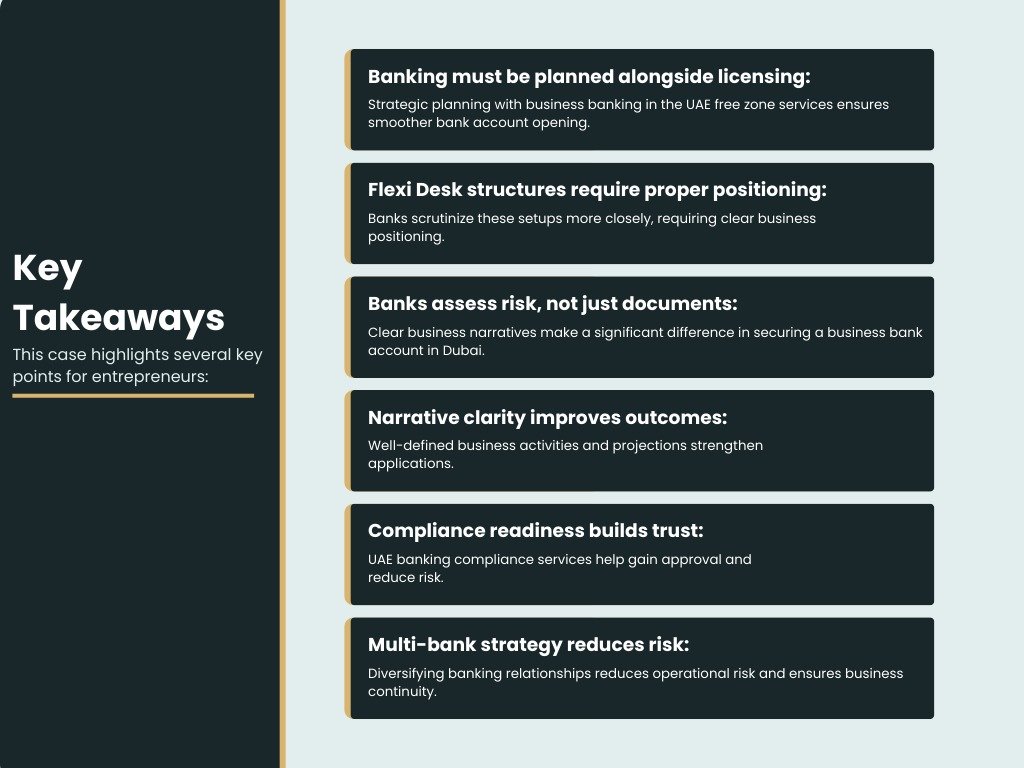

This wasn’t just an issue with opening a corporate bank account UAE; it was a structural and strategic challenge. Many entrepreneurs assume that once they receive their business license, banking will automatically follow. However, UAE banking compliance services and banks assess businesses on different grounds, including:

- Substance vs. perceived shell risk

- Clarity of business model

- Transaction logic

- Geographic exposure

- Compliance maturity

- Economic purpose

A Flexi Desk structure, without proper positioning, often leads to deeper scrutiny. This doesn’t mean rejection by default, but it certainly triggers enhanced reviews. The key question was: How do we make this business understandable and credible from a bank’s perspective?

Our Approach — A Structured Banking Strategy

Rather than rushing into bank applications, we took a methodical approach to develop a comprehensive plan.

Step 1 — Bankability Diagnostic

We started by conducting a complete review of the business:

- Nature of activities

- Business model

- Expected transaction flows

- Counterparty jurisdictions

- Ownership profile

- Regulatory exposure

- Substance indicators

- Source of funds

This detailed analysis helped us understand how the business would be perceived by banks, and it guided our approach to UAE bank account opening for the DMCC company.

Step 2 — Documentation & Gap Analysis

We identified gaps that needed addressing:

- Business narrative clarity

- Commercial rationale

- Transaction explanation

- Supporting evidence

- Operational justification

Banks require more than just paperwork; they want a clear and convincing story.

Step 3 — Crafting the Banking Narrative

This is where many applications fail. We helped the client articulate a coherent story:

- What the company actually does

- Why the DMCC Free Zone was chosen

- How revenue will be generated

- Who the clients are

- Why the structure makes sense

- Expected inflows and outflows

- Growth projections

With a clear narrative, the application became stronger and more aligned with corporate bank account compliance in the UAE.

Step 4 — Compliance Positioning

Banks are more likely to approve applications when they see that a company is ready for compliance. We ensured the client was prepared in all aspects of:

- AML awareness

- Transparency of ownership

- Risk declarations

- Supporting explanations

This AML compliance services UAE positioning greatly increased the likelihood of approval.

The Key Strategy — Dual Bank Approach

Rather than relying on a single bank, we implemented a dual-bank strategy to secure the client’s success:

Tier 3 Bank — For Immediate Operational Capability

Tier 3 banks tend to be:

- More relationship-driven

- Faster in onboarding

- Flexible with structured cases

This allowed the client to open a corporate bank account in the UAE and begin operations without delay.

Tier 1 Bank — For Long-Term Credibility

Tier 1 banks have:

- Strong international standing

- Robust compliance frameworks

- Conservative onboarding processes

We carefully positioned the case and secured approval from a Tier 1 bank, which helped the client establish long-term stability. This step was crucial for building credibility and ensuring business banking in the UAE free zone operations.

Why This Matters:

Many companies apply randomly for banking solutions for free zone companies, only to face rejection. Our approach was methodical:

- Secure immediate functionality

- Build credibility for long-term success

- Create stability through UAE banking KYC assistance

The Outcome

After our structured approach, the client achieved:

- Two corporate bank accounts were successfully opened

- Business operations commenced

- Client confidence restored

- Banking risk diversified

But this wasn’t the end. The client’s relationship with us transitioned from solving a short-term problem to becoming a long-term advisory partnership.

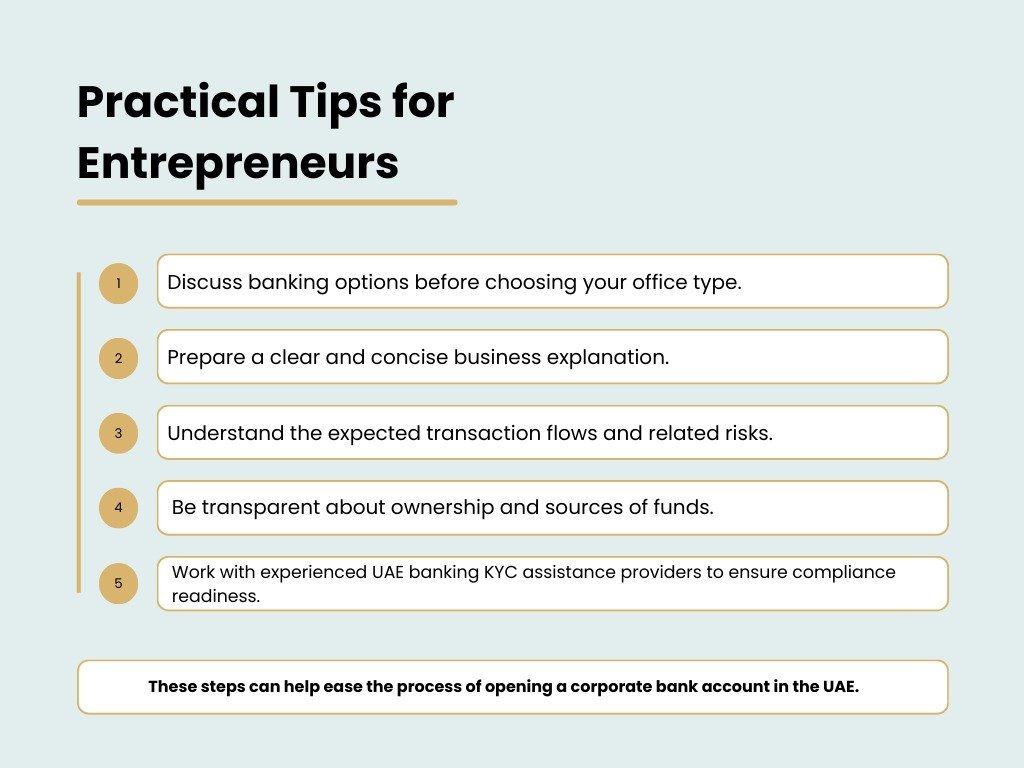

UAE bank account opening for a DMCC company requires careful consideration, and with the right strategy, banking challenges can be successfully overcome.

If you are setting up a business in the UAE, particularly in a free zone like DMCC, consider these tips for a smoother corporate bank account opening experience in the UAE:

Our Philosophy

At Inchub, we don’t just submit applications; we create structured strategies. Our role is to bridge the gap between:

- Entrepreneurs

- Regulators

- Banks

- Compliance expectations

When the foundation is strong, everything else falls into place.

Closing Thought

What began as a challenging situation evolved into a success story, not because of shortcuts, but through careful strategy, planning, and execution. We apply this approach to every case we handle, ensuring businesses overcome challenges and thrive in the UAE’s competitive environment.